|

|

|

Archive for April, 2007

April 30th, 2007 at 07:11 pm

Hmmm, I think I will go back to tracking spending here/sharing more, now that I have more time.

Well, just put almost $150 on the card. Paid the diaper service. (I put everything on the card for rebate money - am due $250 in just a month or so - woohoo!!!).

& since we decided to sign up LM for toddler class this month when I looked up the # I saw the community center had the summer catalog. So I looked through and found oodles of classes for the kids. Good thing so cheap.

One thing BM has been wanting to try is MArtial Arts, and gymnastics. When he turns 4 in the summer there will be lots more options, but there is a little Toddler one, one night a week, we will give it a whirl. Will make it a hectic day, but oh well. I also saw the swim catalog and surfed the web a little as I wasn't as pleased with the community center's swim lessons last time. He's turning 4 and I think really he should know how to swim this summer. The plus side is his preschool got a pool late last summer, and worked with him, and we have a community pool. So we can work with him, and his preschool will too. But I looked up the YMCA (where I learned to swim at 4 or 5) & it was insanely expensive!!! Wow! I think the private lessons offered at our pool are cheaper, and I think it is a very important skill so maybe I will call the homeowners association and see if they are offering lessons this year or what. May be worth it. Or we will just take the cheap community center ones, watch what they are attempting to teach, and work with him I guess. We could do that. We can work with him a lot this summer, it is nice having access to a pool just down the street!

I also have pretty much avoided gym memberships and workout classes since having kids due to time and costs. Last year I was still breastfeeding (hard to get away much more than for work), spent 18 months pregnant the last few years, etc. But the aerobics class is only $2.50 a class or $30/month for 12 hours a month. So I called dh and asked if he would mind terribly if I spent 2 nights a week at aerobics, and a saturday morning too (usually let him sleep in because I am an early bird - well he can still sleep in sundays).

Anyway, he didn't really care or mind, so I signed up and start tomorrow. I have been wanting to get back into it and get in shape, but just no motivation. Shelling out the money and having to go to class 3 days a week, is the motivation I need. $2.50/class - can't beat it. Hopefully it works out!

So 1 class each for us was about $30 each - so just charged almost $150 to the card with that and diapers.

I think for BM we might try gymnastics and martial arts this summer. Most of the classes we have taken through the community center have been so excellent and affordable, I hope the martial arts is the same - he will be so excited. & he can try out the gymnastics too later in the summer. Plus we will be working on some swimming. Busy busy busy I guess. For the long run probably make him choose one or the other, but he has seen karate on t.v. and thinks it is way cool. Of course he tries to imitate crazy gymnastic moves too, sometimes worry he is going to break his neck, so that will be a good outlet too. There's a nice kid's gym down the street from my work, but it cost twice as much. & the martial arts is even worse. So we'll give the cheaper option a whirl and see how he enjoys. As long as we're paying for preschool is probably the best he will get.

Gosh, I don't remember the last time I did something so for ME! 3 days a week for me, to get in shape. Hehe - I am excited. I kind of miss just going to the gym - I love working out and am a gym girl, etc. But just hasn't been in the cards for years. So something like a cheap aerobics class makes me giddy. I have to get on my neighbor's case too. She has a dance studio in her home and offered to teach aerobics to some of us moms on the weekends. I should bug her too, to get on that. Now that would be convenient!

Posted in

Just Thinking

|

0 Comments »

April 30th, 2007 at 02:18 pm

Before forget, you knew I was perusing craigslist the other day (was looking at cars - well at least dh and I both have our own downfalls - which we really do keep to a minimum - I swear - LOL). But while looking at the convertibles, and even considering going for something cheaper and lesser quality so I can buy one sooner (eh, decided against it) I started perusing rest of Craigslist and skimmed the want ads. There were a handful of adds offering $65k to bookkeepers. What in holy hell??? That's how much I made last year 5 years as a CPA - LOL. Anyway, I am looking at the ads and scratching my head. But the interesting this is most of the ads were from CPA firms, and in fact we have been looking for some experienced bookkeepers as well. We just can't find enough CPAs, and well, if we can find anyone who can do the work, as long as the CPAs oversee it, is all that matters. But with not enough interest, we are really upping the ante.

So what does my CPA license and degree buy me today? Maybe a few thousand a year for now, which is good. Definitely a lot more with time and more responsibility. But in the interim, I just have to say if you didn't go the CPA route and you enjoy bookkeeping, go check the want ads. Holy cow! You aren't doing 1/2 bad. I was just telling my mom last night about this since my sister just got her AA degree in accounting. Of course, with no experience, she won't get any of these jobs. But it is interesting. The industry is just crazy right now - and they keep saying like 1/2 of the CPAs are retiring in the next decade. I think it will be nearly impossible to strike a work/life balance in this unfortunate set of circumstances. Sure the pay and job stability is amazing, but the lack of qualified workers is pretty hard to work around all the same - my boss says this was the WORST tax season he has ever had in 30 years, and he lost a lot of clients to retirement these last few years. Of course maybe as so much of the workforce retires, it will kind of work itself out. ???

But anyway, I am not big on lots of responsibility. I would love to just drop back and be a bookkeeper. Frankly, is why I love my job. I have felt like a glorified bookkeeper - paid very well for easier work - in years past. But these days more and more responsibility pushed my way. As long as I have a CPA designation there is probably no way around that - I just have to get used to it. I expect a big raise next year thought - wow! I didn't see anyone paying my job more (in the ads) than $75k which is about what I will gross this year with my bonus. But it is kind of cool to know I could downgrade my job and not lose much income. Makes me wonder if we should demand bigger raises still in coming years. The industry has just been in overhaul, I have hardly had anything less than a 5-10% raise as is, and it doesn't seem to be slowing down - that is the crazy thing.

Well, today is the first day of "normal" in months. I am going to take BM to preschool and leave early to pick him up.

I don't plan to work past 5 all week!

I may even come home for lunch 1 day this week.

& I will sign up baby for his toddler class this month. Might as well, I can break away from work and go with him.

Ah, back to normalcy.

& if the week goes well I might even take Friday off!!! Woohoo. Still have to see how the workload and deadlines go. I have a tax appointment tomorrow too - ugh - procrastinators - LOL.

I think I am going to bite the bullet and apply for credit cards and see how it goes. I am going to apply for one with 9-month free balance transfer and $100 in gift cards and dh is going to apply for a 12-month 0% BT & $50 gift card. I am going with citi card because it seems they are the EASIEST to get a check, and they definitely have no fees, etc.

My plan is for next year for both of us to apply for Discover cards so we can do a BT to the old cards and extend it out for another year.

Then we're going to pay them off AND cancel the cards, and see what that does to our credit score. & then cool it for a while. I couldn't play that game on and on and have a ton of cards. We were originally going to just test one of our credit scores, but we decided it really didn't matter. I don't know. Last time we borrowed a lot of money, paid it off and closed it in a short time our credit shot up to the 800s so overall I am not too worried. But we'll definitely keep an eye on the score and proceed slowly. The gift cards (Target!!) will be a nice perk! I was going to let dh use one to get a game controller for the PS3 ($50?) but he just found a way to get one for free - so go dh.

The unfortunate thing is that I have to apply for the cards, get them, and make a purchase, to get the gift cards. Then will pay it off and do the BT. So no cash for a couple of months. I read the blog instructions and the fine print on the cards like 100 times to be sure, and now I am ready. How exciting! I hope we both get $5k - $10k, but who really knows... I'll let you know!

I used to think it was so awesome to be debt free, and lately I keep saying, well "I am debt free except the loan that I choose not to pay because I make more in the bank." But you know what - I am just going to say I am debt free. This does not count - LOL. I am going to borrow the money, put it in the bank, and not touch it. Or should I just start saying I have all good debt for leverage. It's funny when I joined here I was like, I don't want to be wealthy, I just want to live and retire comfortably. I guess that is still my goal, but I am sitting back and thinking about the big picture more. Where once I would not consider carrying any debt it is quite a mind-shift, and wealth-building attitude, to use low interest debt to our advantage.

I feel confident as I have never paid a credit card fee in 14 years of card ownership. Pay the bills on time, read the fine print, just doesn't seem very hard. All the same I still have a fear, what if I screw up - the fees could be nasty. So we'll see. At least we'll get some gift cards - LOL. I even told dh I was going to put the BT transfer info with our will stuff so if something happens it gets paid right away. I can just imagine our family's surprise if they found we had $20k in cc debt - what the heck??? LOL. & I will make sure dh knows when the bills are due and where the money is in case something happens to me. Maybe a little overkill, but just don't want it to bite us in the ass for ANY reason. Not even to our estate if something happens to us- wouldn't give the credit card companies the satisfaction of squeezing a dime from us for any reason. Oh yeah, I probably hesitate because of my overall disdain for them, but all the more reason to take free money from them I guess.

Posted in

Just Thinking

|

1 Comments »

April 30th, 2007 at 02:49 am

Um, apparently the freeway melted and collapsed from a giant tanker truck fire. Who knew that could even happen? Luckily was 3am - sounds like so far no one was hurt?

Text is http://www.pleasantonweekly.com/news/show_story.php?id=134 and Link is http://www.pleasantonweekly.com/news/show_story.php?id=134

Yikes!!!!

ETA: Still say no one was hurt or killed (except truck driver who walked away from the scene - he isn't so bad off...).

Amazing.

Posted in

Just Thinking

|

1 Comments »

April 29th, 2007 at 03:05 pm

Oh yeah, it is a bad sign when you have to turn on the a/c in April. Yikes. It was a hot weekend and we waited it out, but last night it was up to 85 in the house so I turned on the ac for a bit to cool off the upstairs for the kids, before bed. Good move since I later opened the window but the neighbors were LOUD last night, and quickly closed the window - hehe. The 10-15 minutes of a/c did the trick and kept the house comfortable for the night. It's 77 in here right now and quite comfortable, as long as I don't do too much work in the house. Was over 90 outside yesterday - ick. The summers where it doesn't hit 100 degrees until July, I can deal with. But sometimes it starts hitting in May, and I am getting scared it will be one of those LONG summers. Hopefully it will cool off for a bit - I really rather have 1 more month of no a/c! The electric bill has been so nice and low!

Yesterday was REALLY nice. Dh had wanted to go to the Scottish Festival, which was quite expensive really. I told him I didn't want to be too stingy and cheap, but since we are going to Monterey next weekend... So we decided to go to the zoo and Fairytale Town which we have memberships too. & you would be proud of us. We packed up a lunch. There happens to be a pond and park between the zoo and Fairytale Town and so we decided to hit FT first, stop and eat lunch ,and maybe run by the zoo for a bit - it is very small.

Anyway, the heat was a bit much as the day progressed, but overall a very cheap and fun day. Kids had a blast.

The little FT also had a promotion where they are going to put in a "yellow brick road" and you can buy an inscribed brick for $100. Would love to to so - I think that is cool. Will have to think what we want to inscribe in it. For a good cause and all.

Anyway, for the ever present truth that less is more to kids, I had to share this. Fairytale Town has a few farm animals and slides and stuff to climb in. A fancy playground I guess. But they have this thing called the "crooked mile" which is basically a little raised path that winds round and round. So when we got there I plopped down and let BM run through it about 10 times. It might as well be a fancy roller coaster as far as he is concerned - the kids just LOVE it. Dh and I have always scratched our head on that one - who knew something so simple could be like the main attraction? LOL.

Here's a glimpse:

& then where we had our picnic lunch:

& the big duck who tried to grab my food. I was a little scared of him, but started snapping his picture and he ran off - he didn't like it - LOL. I guess he was a duck - I don't know - some big fellas.

We figured we wore out the kids real good and they would nap all afternoon and maybe even sleep well at night, but the plan backfired. They went on nap strike and were extra grumpy to boot, plus we were exhausted. Oh well. Baby had another awful night. Ugh.

We actually went to the SF zoo last year once and it was quite cheap, but the food did us in. So we are thinking about it for this year - we just need to pack up a lunch and go enjoy - the zoo even has free parking. I guess gas will be the pricey part, but is such a nice zoo. All we have to do is rein in the food costs to make it a pretty affordable excursion.

Posted in

Just Thinking,

Picture Project

|

6 Comments »

April 28th, 2007 at 02:43 pm

I have learned a couple of big lessons lately that are leading me to tweak my goals again.

I think I can sum them up into 2 lessons:

1 - The answer to most financial questions is: it depends. No one-size-fits-all!!!

2 - Doing something without truly thinking it through and looking at the big picture (like doing it on a gut feel) is not smart.

My gut feel used to be I wanted a lot of cash and no mortgage, etc., etc. But I was falling behind on all my financial goals by being so short-sighted about the BIG picture.

I've been coming to this realization slowly over time, but I finally gave into the other side of the great mortgage debate and completely change my tune. I no longer am paying an extra dime to the mortgage. I don't see the point. I decided to change my tax withholding because I was a little behind. At first I was frustrated as it significantly compromised my savings goals. & then I looked at the stupid $30 extra mortgage payment and decided I would commit that to retirement instead. Much smarter! Before I looked at it as a forced savings, a small amount I wouldn't bother with otherwise. But forced with such a huge budget change, I thought, gosh, I have been saving that $30 no prob - why not just put it to retirement instead. I can commit to save a small amount. & that is huge - a huge change in my thinking just over the last few months. Getting away from the so all or nothing thing.

We also have formulated a plan for our cash savings. We are going to keep 3 months bare minimum expenses and that is it. The rest - again to retirement - much better returns in the long run. We are losing out on so much earnings potential wanting a lot of cash in the bank.

In my new thinking I am just able to weigh everything with our goals and make decisions now. Vanguard dropped their fees so the $50/month I have been adding in a slow attempt to erase the fee of 1 fund (thought it was screwing up my allocations - and was why I was doing it slowly) - well I no longer have that need. I dropped the investment plan yesterday. By doing so we are on track to meeting our 3-month EF by December, $1k to invest, and the $1500 to do my final ROTH conversions. No more money to retirement this year, but with a $13k contribution from my job this year, just makes sense. We can go into 2008 with a full e-fund, an investment account started, all ROTHs, and can contribute heavily to the ROTHs in 2008. Woohoo.

Anyway, many circumstances have changed this month, but having the big picture in mind it was easy to make the appropriate changes and work with them.

Anyway, besides 3 months in expenses we will be adding $100/month & my overtime to savings for bigger purchases (cars and house maintenance) but should be plenty, with these interest rates anyway. We will start investing a very minimal amount in a balanced fund, since my new-car horizon is so far away. & for longer-term stuff. & then hoping to set aside about 8% to ROTHS. But of course, any unexpected windfalls will got to max those out. So I think the odds are high we can max out next year and still make decent progress on our savings. My gut wants to max out the ROTHs, but realistically, we don't need a 25% retirement contribution next year. Not at cost to all else. We'll get there in a few years. No hurry for now. Having more than enough for my own ROTH, on one income, sounds nice and dandy. But if anything extra comes along... It is reachable to fund both, all the same!

Some reasons I have changed my tune:

1 - thinking about our time horizon and how we have a 40-year plus investment horizon for investments. Longer horizon means more time to ride out the wave.

2 - Even if we take the full 30 years, the house will be paid off in our young 50s or well before retirement, no need to stress about it right now. It will be so much easier to make extra payments in a few years and will still have a significant impact - if we our making all our other goals.

3 - Our interest-rate is low and we will have the mortgage deduction (effectively making it lower) for years to come.

4 - I feel confident in the ability to earn twice as much over the long haul - 8 - 10% vs. the effective 4-5% mortgage interest rate.

5 - Yup, 8-10% because in the ROTHs it is all tax free earnings! Makes it the no-brainer.

6 - Over 90% of our net worth is in our home - we need to spread out our investments.

7 - Our mortgage is very reasonable and low-cost for the area. If I had a huge windfall I would have NO urge to pay off the house. I find small monthly payments much more manageable. I NEVER got the idea to pay off a house with life insurance, but I guess being the sole breadwinner I wouldn't - LOL. I look at life insurance as more of the retirement contributions that my dh would have made in life. Of course if something happened to him I would downsize the house anyway, may be able to pay it off in that case. On the flip side, the mortgage is quite huge at $215k. It would take a big effort to significantly pay it down early, at all costs to retirement. Instead I expect we will have the income in a few years to pay it down faster and in the end will still pay it off just as fast as originally planned. But will have lots of money in the bank, earning a nice return, to boot.

8 - I still can't get past the idea that my house could flood away or we could get sued for something stupid and have it taken away, but that our retirement is so safe from creditors, bankruptcy, lawsuit, etc. I just do not feel warm and fuzzy about having a $600k asset paid off. Frankly, it scares the hell out of me to sink all our cash into the house. If it was a $200k or $300k house I would feel differently. It's all in the sheer size and weight in our overall wealth I guess.

& as far as cash:

1 - job security out the ying-yang

2 - Plenty of insurance on all fronts

3 - Plenty of 0% credit options as well as plenty of well-off family to fall back on (loans) if we hit some really horrible times like the house flooding away or major medical bills.

So though I really want to hoarde a lot of cash, we probably could hardly be in a better position to not really need it. We just have a lot of options. So we decided to stick with the 3-month expense thing. The odds I will be out of work for more than like a day are just really slim to none in this market, and my job is quite recession-proof to boot. ( I exaggerate a tad, but not really, I could go find a job in a day - it is just crazy in my field right now). Disability actually would cover all of our bills - both the short-term and long-term (disability), and we have plenty of life insurance and all that. Medical is the big unknown for now, but we have low deductibles at least. I am starting to think we should keep a little less in the bank and try to pay for the higher premiums again next year. Might just be worth it to keep the costs controlled, even if the premiums are insane. Something to consider.

Anyway, overall it is amazing to me how much my thinking has changed in just the last few months. But I think we are looking at the big picture a lot better and are maximizing our wealth.

I still can't believe car is paid and we are so on track to so many goals this year. Though the year is young and anything can happen, all the same.

All that and a HDTV!

But setting goals and being focused has sure paid off tenfold... I had the focus before, just really not any tangible goals. What the hell were we doing anyway? LOL.

Posted in

Just Thinking,

Budgeting & Goals

|

2 Comments »

April 28th, 2007 at 01:47 pm

Hey, I went to get my car yesterday and no charge - they'll just bill me when they finish the work - how nice. I called to ask if we could cancel the part order and call around some of the dealers and at first he said yes, but called later to say it was too late. I figured we'll just replace it. But maybe a good lesson to call the dealers for a second opinion at the least, you never know. Maybe this is a common problem with a quick fix.

Anyway, reminds me how this mechanic has annoyed me in the past with annoying assumptions! He'll look at the car, fix what I bring it in for, have it all ready, and then when I pick it up he says "you need this and this done too. Bring it back later." But not knowing us better I guess made the sweeping assumption (maybe the more common choice) that we rather wait and save up the money and bring it in later. In reality I want it taken care of while I went out of my way to go carless for a day or 2. Gah. It's just my pet peeve. In some cases maybe it paid to wait. But anyway, after a few times I told him, look, I rather get it all done now. We have such a great long-standing relationship with our mechanic back home and he is very honest about what is critical and what can wait, etc. So I have been trying to get this info more out of him. But if it really can't wait more than a couple of months - please just do it now!!!! So I think he is getting it. Of course, he still hasn't 100% learned. Am I sure I really want to fix my power locks now? Um yes - it is driving me batty - I left all the doors unlocked yesterday because I completely forgot - at work - not the best area. I need my locks!

Anyway, this also happened at the hospital. We were in for dh's ear appointment after he started losing his hearing suddenly. Overall something big and major - right? But the doc looks at our chart and says, oh, I would usually send you to the PT, but looking at your high co-pay plan, oh, you are just better off waiting a few days first - it might go away. In the end that was better advice, and it did. I am glad we didn't output the money. But the assumption that we should put off some procedure because we probably don't have the money? Ugh. There it goes again. It's his hearing!!! I will pay good money to get it fixed!

Geez.

I just find it interesting the assumptions made. If we had a better plan (which by the way cost another $300/month!!!) and were wearing expensive clothes would we have had an unnecessary PT appointment? Hmmmm. It only would have saved us $25 on the co-pay but we'd be out another $3600 all year for the premiums. So yeah I would rather have that advice on the other plan - LOL. People are funny.

Posted in

Just Thinking

|

0 Comments »

April 27th, 2007 at 04:50 pm

Every time I see "Money Karma" it reads "Monkey Karma" to my eyes - always cracks me up.

Anyway, dh needs to fiind the money for the t.v. & well, he just got a video job - woohoo. Out of nowhere, didn't have to look or anything. Well, he did some work for a client of mine last year, and they want him to do some more - editing some old videos, transferring to DVD and putting on a continuous loop so they can play in their lobby. Will probably net $200-$300 for that, whenever they get the details worked out.

My mom also offered the same when I told her about the t.v. purchase - they have a lot of old stuff to move to DVD. But you know, it's fam, you don't want to charge them. But I am starting to think he should take up the offer. He hasn't done anything yet and won't be a priority until cash is a reward. Just the way it is. Ask how far he is along on OUR own home videos - LOL. We got a "first year" video for child #1 & that's about it. Which reminds me though he did say he wanted to devote some time to that this summer. Hopefully he can make progress on all of these things now that I am much more free!

In other news, my dh is quite happy to spend his days playing video games and watching t.v. He is a real homebody. I am pleased that is changiing (maybe he is a little stir crazy - I don't know). He wants to go to the musemum and a Scottish festival this weekend. ???? Who is this guy and where is my hubby? Hehe. Well, we'll see...

Posted in

Just Thinking,

Budgeting & Goals

|

0 Comments »

April 27th, 2007 at 01:50 pm

Text is http://www.iwillteachyoutoberich.com/blog/cheap-versus-frugal and Link is http://www.iwillteachyoutoberich.com/blog/cheap-versus-frugal

I thought this was an excellent article (on cheap vs. frugal). An old article, but got directed to this website by househopeful's blog yesterday, and enjoyed.

Anyway, part of the distinction between cheap and frugal, in this article, is that cheap people will screw people over for a few bucks and frugal people in general are a little more generous, and have more to give. I thought it was a very interesting addition to the cheap vs. frugal list. I was also thinking about it in terms of us. We used to be very generous with our money. We used to donate all of our used stuff, and be generous with gifts, etc. Anyway, in recent months we have moved to the opposite end of the spectrum. I honestly can not say this has made me very happy. & reading this article kind of nailed it on the head for me. You know, maybe we were stupid with our money before, but I have been thinking of those studies where they show money makes people more mean. LOL. I have been really grumpy lately, thinking about money too much, etc. I think middle ground is probably good. So thinking through all this, I just agree. For the most part the frugal definitions in this article describe us to a tee and I think is something more to strive towards. Anyway, I also looked at this extreme penny pinching as pretty temporary to get back on track. & as we near our goal, we'll probably do what we can to get there. But once we get there I think we really just need to chill out. I find us spending an inordinate amount of time to save a few dollars, in a few cases, which just does not make any sense to me. When we made minimum wage it made sense. It no longer makes sense. Not worth the time and stress I guess, we have the luxury to let it go. I can't say we are any happier becoming extreme penny pinchers, actually, quite the opposite.

Anyway, just kind of my thoughts of late that I haven't really formulated into a blog yet. But reading this made me ponder it a little deeper, and find the words to what I had been feeling on some level.

Oh yeah, and I am enjoying this guy's blog too:

Text is http://www.mymoneyblog.com/archives/2007/04/our-spending-breakdown-for-the-last-year.html and Link is http://www.mymoneyblog.com/archives/2007/04/our-spending-bre...

I really enjoyed the comments on this post, because the guy started getting reamed for not having the "10

% tithe" category which I moan and groan about lately myself. I have argued that for myself, giving to my friends and community and such is so much more rewarding than setting aside a cash percentage for charity. But anyway, someone really echoed my thoughts here - they thanked the guy for his blog and what a great public service it is. I guess to me it just angers me that such contributions are written off as not important. Just giving of yourself in any way, shape or form is just very important. It does not have to be with cash. I guess for me putting a percentage to tithe just, I don't know, it doesn't jive with me. & it is amazing to me to see so many in the personal finance community make such a large commitment with their income. Anyway, I don't want to start a debate or seem judgemental. If you are happy with your tithing situation so be it. I almost don't even want to go there. A very personal/touchy thing I guess. But I think it is important for people on the fence, or are unhappy with giving so much cash, well, to know that there are so many other ways to give. & in the great debate if a blog is a charitable cause, I would argue it is. But seriously, try it, help a neighbor, a friend, acquaintance, and see how enjoyable that is. It does not take a pile of cash to be a giving person. Ah, quite the contrary. I guess too I like the flexibility of giving when it feels right, rather than some sort of obligation. If I had given the token 10% I could not have helped a dear friend financially last year. But when the time arose I was able to help. & I know the money went to a wonderful cause, whereas with charity it often gets fuzzy. I know devoting my time to certain charities I can see the difference it is making, where it is harder to see with the cash contributions. & so it goes, I guess my attempt to reinforce the value of giving in any way, shape or form. If you don't have the cash to give, there are other ways to be a giving person.

I guess it is all a big balancing act. When you get too extreme, it just gets ugly. I think we will work on some middle ground between frugal and giving, and not cheap - LOL - in the times ahead. Still working on that right balance I guess.

Posted in

Just Thinking

|

2 Comments »

April 27th, 2007 at 01:34 pm

$20 challenge:

$6,863.14 - Balance 4/16

$ 62.38 - Interest for April

------------------

$6,925.52 - Balance 4/16

------------------

This is how much money I have accumulated since 1/1 by doing things a little differently. Gosh, it is amazing.

Starting to accumulate significant interest. Gosh, wait until I cash out a credit card for the interest too.

Posted in

Just Thinking,

|

0 Comments »

April 27th, 2007 at 01:25 am

Everyone around here is burned out and doesn't intend to work this weekend. But frankly, I am so behind AND I want next Friday off, I didn't mind coming if for a bit. Though I was worried it might be a long saturday of working.

Anyway, all the problems cleared away and I have been whipping out payroll stuff left and right - more caught up than I imagined I would be today. Monday is the deadline!

Basically, I don't think I have to work Saturday!!!! Oh my. I don't think I will tell dh yet (just in case something comes up). A nice surprise for him and the kids. The kids have been very patient and well, but I think they are getting pretty sick of me working long saturdays.

Anyway, honestly, I probably rather come in a bit and get a bit more caught up. I don't have to work a monster day or anything. & even if I stay home I am WAY behind in my writing for the week.

But if no one else is going to be here, why should I? I think I will just be lazy, take Saturday off. & hope I can get a lot accomplished Monday through Thursday next week.

Ah, a 5-day work-week. WHat's that????

I know next week will be a little crazy, maybe the week after with 5/15 deadlines (gosh, these deadlines NEVER end). But I am hoping to work out a schedule with more free time to do some writing during the week and some exercise and such. So the weekends can truly be enjoyed. We'll see...

Yup, property tax returns due May 7 (ugly since I am behind on some of the accounting which would have the info I need) and I have 1 audit in particular I have to square away by May 15 so I can do their non-profit tax return. Yikes. Since I have been kind of pushed more into a management role I guess there is no escaping the endless deadlines!!! In the past many would pass without me having to break a sweat.

I am still dreaming of cutting back my hours. We'll see, hopefully I will catch up significantly in May and then take a breather. I can definitely say the WORST is over for the year - phew. That's something!

Posted in

Just Thinking

|

1 Comments »

April 26th, 2007 at 06:56 pm

I asked dh to get the ingredients for this a couple of weeks back as I was craving. Luckily he spoils me rotten because I decided I really wanted something wonderful and sweet - like this cake - last night! But forgot when I asked for ingredients that the sour cream. It probably would have been okay still except dh had used it for cooking something else in the meantime, but he ran out to the store for me. I was way too tired when it was finally ready about 9pm last night, so we ate it for breakfast - yummy. This is just the most divine & easy cake to make. Don't ask me about calories though - I'm sure there are more than you need! Oh yeah - and heat in the microwave a good 10-15 seconds before serving. It is just so good served warm!

INGREDIENTS:

1 box yellow cake mix

1 cup sour cream

1/3 cup oil

2 tsp. ground cinnamon

2 Tbls. brown sugar

1 cup chopped pecans

1/4 cup sugar

1 cup powdered sugar

2 Tbls milk

4 eggs

1/4 cup water

PREPARATION:

Take 2 Tbls. of the cake mix and mix with the cinnamon,brown sugar, and pecans; set aside. In large bowl, blend cake mix,sour cream,oil,water,eggs, and sugar. Beat on high speed for 2 minutes. Pour 2/3 of batter into greased and floured bundt pan. Sprinkle the cinnamon sugar mixture in the center of this and spread remaining batter evenly over this. Bake at 375� for 45 minutes.

Cool in pan for 25 minutes. Remove from pan.

To make glaze; Blend powdered sugar and milk together to make a glaze. Drizzle over cake.

Posted in

RECIPES

|

1 Comments »

April 26th, 2007 at 04:31 pm

I came to the conclusion a while ago that our very old cars were much better purchases because we could afford so much more quality.

& anyway, today I am left feeling really annoyed with our van and wondering if we sacrificed too much quality for something "newer."

I am just aggravted. I am not sure what the final bill was - should have asked - but fixed the window and the mirror. & the oil change for convenience. But the power locks is something entirely different (I figured it had been related). Though I am glad it is not an overall electrical system malfunction, the part that needs to be replaced still is about $350. Mechanic said maybe I should just take it in to the dealer, might have to anyway to program it. But the principle really gets to me, that they make cars these days that only the dealer can fix. I ain't playing the game. I discussed it with dh and he said, well, odds are the dealer will screw you over. True. Kind of my feeling. Mechanic is old friend of family, on the contrary. So we will have him try to fix it - but the part won't be in until next week. In the meantime it is such a PITA to not have power locks. I would not mind so much if there was keyed entry on the passenger side, but there isn't. & we can't really figure out how to keep the back locked, without power. Considering we live in auto theft central, I really want my door locks back!

I think the grand total when all is said and done will be $1k. Absolutely ridiculous. I have just never had such a new car before and NEVER had these kind of stupid repairs. Is it too much to ask that the power windows and power doors last more than a couple of years? Have I ever spent $1k on car repairs in one service? Probably not? My last cars were old, but they had power doors and windows that worked for decades!

Overall I guess my standards are pretty high. HAven driven a 20-year-old Toyota with little problems, and the same with our Saturn, and our cheap little Escort, I am just not pleased with the Dodge Caravan thus far.

Oh well, at least the mirror is my fault - I broke it. There is something.

Well, we'll see. Have to take it in again next week when the part arrives. & then schedule for service at the dealer too. Times like these it is just nice to have a 2nd car and a spouse who doesn't work - to chauffer me around and overall not too much nuisance to my work day.

Well here is to better car days...

I haven't completely ruled out selling it, pocketing the change, and buying my camaro instead. LOL. Or even just an older Japanese model.

ETA: Since I can't comment I will comment here - LOL. Thanks for the tip - yup - we have the 05 Grand Caravan. Very Interesting. I will have dh call around and see if we can hold off on the part in the meantime - if he can cancel the order!

& that's what I mean - what's the point of buying new if you can't afford quality? Or you don't want to spend it anyway. Oh well, I feel we are on track to buy better next time. I should just feel lucky the Ford has held up so well, it was dirt cheap! Helps offset it a bit.

Posted in

Just Thinking

|

4 Comments »

April 25th, 2007 at 06:36 pm

I need to log into my online MMA more. GMAC is now paying 5.3% APR!

I've been looking at c.d.s and treasuries now that our e-fund is about at its goal, and well, don't see the point for now.

I tried to pick a bank this time around that had a longer history of good rates. So far very proactive in raising rates (from 4.97% in just a couple of months). Since high yield is not everything to me (much weight on history/security of institution, FDIC, cusomer service, etc.) I am pleased I found a decent compromise for all that I wanted in a bank. For now anyway. Yeah, the subprime whoas are something to consider, but for now I will take GMAC any day over most the fly by night online banks. I do wonder if that has anything to do with more attractive rates though - haven't been keeping a close eye on rates overall...

Posted in

Just Thinking,

Budgeting & Goals

|

1 Comments »

April 25th, 2007 at 04:32 pm

I really wanted to take my car in next week, since it is crazy this week, but I started worrying as the electric problem seems to be spreading. Fearing if it got worse if it would cost more to fix.

Who knows, but we dropped it off today. Usually when the car goes in the shop I Tend to drop off the fam, go to work, then pick them up and get the car in the evening. But I thought, this is dumb, they probably need the car more anyway, I'll just be at work. So we dropped off the car and I got dropped off at work. Plus since I usually have to leave 4:30 to pick up BM (have not done so in months), it isn't so bad if dh picks him up first and then gets me - will be closer to 5:15 or so - buys me 45 minutes at work - which is good. Anyway, crossing my fingers the diagnostic is not too bad. WIll replace the side mirror and get an oil change while it is there. Not very frugal or cheap, but it is convenient and that wins hands down - LOL. Said I'll get it back tomorrow (unless it is something REAL bad). Oh yeah, fingers crossed. Of course mechanic looked perplexed as car is so new. YEah, that is what I was thinking. "New" car, already screwed up. Bah!

So yeah it is crazy here but I have "senioritis." I am SO itching for vacation and time off I guess. I am a little bummed because I have been ITCHING to go to Monterey and do something fun with the kids, on a Friday to avoid crowds. So I was thinking weekend of 11th, but BM got invited to a birthday party he really wants to go to. I vote Monterey still - LOL - but dh and BM vote party. Bah. So my first FREE weekend we will probably be driving and all that. Though I really look forward to the idea of a 4-day-workweek next week all the same. But then again, just so behind, wanted to have a nice full week to catch up a bit after this deadline. I could postpone Monterey to the following weekend, but I am driving down the Friday after that to get my tooth filled and want to avoid 2 weekend trips in a row. Oh well, decisions decisions. Regardless, no Saturday working in May, 1 holiday, and probably 2 days off to boot. One for as filling, but I tacked it on the holiday weekend so I could still drive back home and bum around for 3 days - LOL. Monterey will probably be decided at the last minute. I just don't know if I can take next Friday off. ???

I really wanted to lose a good few pounds before the cruise, but ain't gonna happen - LOL. Then again, weather has been nice, things have been slowing down, have been resuming the afternoon 1/2 mile walk at work in the afternoon. Maybe it is only 1/4 mile, but whatever it is is better than nothing. Last year I was a lot better about walking to get the mail and walking to the park/pool in the evenings. We have started resuming that somewhat, but after this week when I resume a more normal work schedule I can commit to more walking, and add some video workouts to the mix. I think I weigh about the same as last summer when we went to HAwaii, but I was in much better shape. I just feel flabby. I still have a good 18 baby pounds to attack, but have just been so wound up in financial stuff and work. HEre's to summer. Hopefully I Can tone up a bit so I Feel less self conscious come cruise time. I actually look forward to the amenities on the boat though - I love gyms, I just don't find them worth the expense these days, especially knowing I really don't have the time. But maybe the cruise gym will motivate me. & I want to be a little more in shape so I can maybe go on a bike ride or a hike, or hit cruise gym without keeling over - LOL. It was funny Sunday but we went out shopping and such and I Was exhausted. I frankly couldn't remember the last time I did much more than sit at a desk. So it is nice to get moving. Well needed.

Today I paid off the TV and its new beautiful stand. Dh picked one out and it is absolutely gorgeous - I love it. He did good. I was wary I would hate it - LOL. Anyway, between the 2, and taxes, $1300. I paid it. I also have to transfer $500 out of savings to pay the dental bill. (planned, short0term savings, actually $75 under budget which will help for filling). & after that we are at about 1/2 our budget for the month. Lord knows how. Dh did STEALLAR on the groceries this month and driving his car more has paid off in the gas department. I have had leftovers out my ears too - just lots of leftover lunches - no sandwhiches or BK runs. At this rate (knock on wood) I think that we will have enough extra in there to pay the mechanic. ???? I have about $350 set aside for that and my filling, before this great under-budget month. I think in the end it might buy me another $200 at the least. We'll see. I know I paid one grocery charge and one gas charge on the other cards already - ahead of schedule. But still, doesn't explain how we are having such a good month. Last day of credit card cycle is Thursday, all the bills are paid, dh knows better than to spend another dime on anything other than necessity - LOL - etc. But then again anything can happen. But I am in a good mood about it all. Just hoping the car isn't so bad...

I will have to dig out old invoices and see how much my last filling cost. Hmmmmm. I had one replaced a couple of years ago. I just don't remember it being that much.

Oh yeah, in other news, the fam may go to Florida in October. Another all-expense paid trip. Spoiled spoiled. As it turns out, dh told his mom about the windfall from my parents, which I was not happy about. So great, he didn't say how much, but his mom guessed upwards of $20k (I guess assuming the free gifting thing). So I was REALLY annoyed with dh. His parents are really generous, and nosy. None of their business, and I can just see then getting on our case about our finances if they think we just received $20k and are still budget like we are broke -LOL. (Oh yeah - and the TV to boot does not HELP!). So we had been discussing Florida next year to visit his grandfather, at an age the kids could enjoy Disney World. But he brought it up one day and his mom got on a kick they need to go throw a big 80th birthday party for GrandDad. Great, that is nice and all, but not in our budget in the LEAST. & it just came so out of left field. Why not until we brought it up we were planning a trip? I don't know. So I was really resisting. For one, it is a big deadline at work and they wanted to go for 6 work days. I guess I am just mean, but dh's sister has a baby due that month. I don't see why we just can't wait until next year - so they can go - and we have more time to plan, etc. I mean I need more than 6 months please to plan for a trip for 4 to Florida. Pricey! I don't care if we all crowd in Grandpa's house - the flight will still cost an arm and a leg - LOL. So anyway, I Was resisting because I figured MIL gravy train was out in light of recent events, and also because I refuse to use 6 days vacation - I already got my vacation planned for the year. So I pretty much told dh if he wanted to go AND his mom would pay, fine. I didn't want to be the 80th birthday scrooge. I kind of just wanted him to leave the baby too - but part of the thing is they have never met him. So anyway, in the end it all works out because dh's mom said if I didn't go, they could all share a timeshare condo ("free") and she had 4 free airline tickets anyway. (baby can take a lap). So trip is paid! To boot, we have Disney World tickets from 2000, our honeymoon, we bought a 4-day pass and I hurt my necj - don't ask - LOL. I think we only used 1 day. ?? So dh and BM basically have 3 days of park hopper tickets to use, and frankly I Am glad to be rid of them. Right now they are just sitting in our safe saying we need to fly to Florida to use them - LOL. So they will probably fly to Florida and all that and leave me, but I Am okay with it. The tickets though are just the icing on the cake - FREE trip. LOL. Of course, I know better. A few hundred dollars probably in eating out and expenses and such. But oh well, sure beats flight and hotel for 4 for a week - my word. I am also kind of annoyed because they just have to be there on the day of his birthday. I just don't get it. if they postponed it a little bit I could have flown out for the weekend or something, but has to be the weekend I have to work - just a big deadline - there is hardly a way around it. I just don't get the draw of the exact day. If someone wants to throw me a big bash the week before or after my birthday, okay with me! But I am not really feeling the trip all the same. HEck I might get a week all to myself at home. Crazy! I wouldn't know what to do with myself. & well if I we don't have to save our pennies for a Florida trip next year, what a load off for me. Phew. I think this could work out nice.

Posted in

Just Thinking

|

0 Comments »

April 24th, 2007 at 04:57 pm

Text is http://money.cnn.com/galleries/2007/pf/0702/gallery.median_income/index.html and Link is http://money.cnn.com/galleries/2007/pf/0702/gallery.median_i...

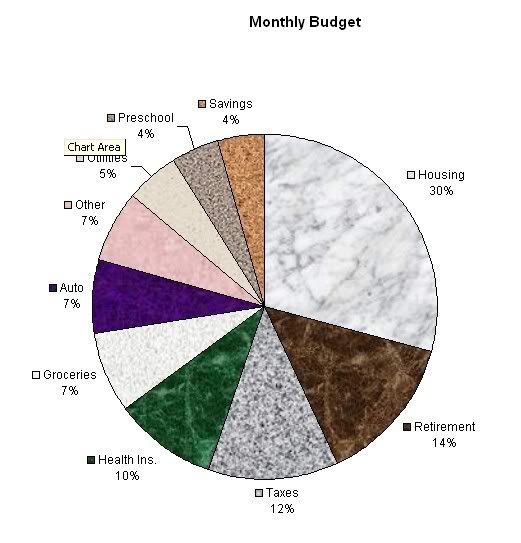

I don't know why, but looking at this article made me want to make a pie chart of my own - LOL. I play with percentages a lot, but never thought to put in chart form. I played with excel and figured it out pretty quickly (learned how in college, haven't done a pie chart since I believe - LOL).

Anyway, I cam up with this.

I think it's perty. Some things to note, housing includes the gardener and other maintenance. Not all fixed expenses. Haven't had the gardener long and would be the first thing to go if needed. I am impressed with the auto percentage - gas, insurane and budgeted maintenance on 2 cars. No payments (as of last week!). I laughed at the thread in the forums about the 8yo car with 85k miles. I think dh's car is 6yo with 65k miles and I figure it has a decade left in it, easily. I still consider it brand new, but I guess for me it is pretty new. But though we don't plan to replace either car soon, most of our 4% savings (and interest it earns) is earmarked for future car purchses, so you could consider our car % at 10% or so (7% + 3% - most of savings).

It surprised me what a chunk our taxes are since we pay so little in income taxes these days, but most of it is social security/payroll taxes (about 8%). I put the property taxes (& insurance & HOA and all that) with the house.

"Other" is all of our other insurances, gifts, donations, medical co-pays (can get pricey), subscriptions, clothing, our allowance (I should have put that in - it's about 1.4% of all expenses for our own splurges). We rarely have enough for ALL this stuff, but I based this graph on my wage alone. Making extra money on the side helps us to find money for all this stuff which we could otherwise live without I guess. Well, ideally we like to divide extra money between the "extras" and adding more to savings.

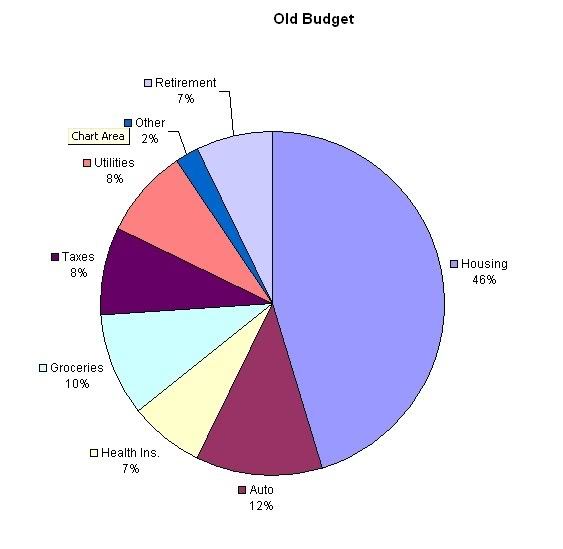

I didn't have the time to pretty up this one as much, but decided to do a graph about where we were at when we had our first child.

It's interesting how different it looks. Housing was a big chunk, but less than we thought it would ever be growing up where we did. I notice over time as our health insurance skyrockets, we shift a lot that was our mortgage % to taxes and health insurance. I expect our taxes to get pretty ugly in the future.

Today we have A LOT more for both savings and retirement. I think that is why when my dh first stopped working we looked at it as very temporary. These days I feel more and more we can do it for the long haul. I never expected to get such large raises in such a short amount of time, so we have definitely upped our lifestlyle and tried to enjoy a little as well.

I figured I would share. It is too often that people will look at someone and say, oh they had it easy. I think I get that a lot more since we have suddenly found a lot more financial comfort. Bigger wage, sudden influx from our parents, etc. But this was not what our situation is when we first made the 1-income leap. It was pretty dang tight. There were many years we never considered having cable or a gardener or the like. But with time I guess things change. I just hope all of us can say the same. With time we should all find more comfort in our life, by taking care of our finances. Slow and steady wins the race!

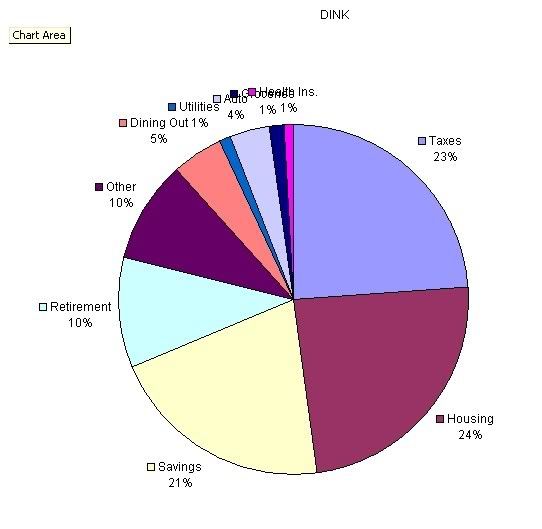

Of course I miss these days (DINK = double income no kids), but saving heavily when we could, really paid off.

Of course I'll take the kids, and added financial strain, any day...

ETA: Oh yeah - sorry I can't seem to reply to my own blog from my work computer - lord knows why. So though I tried to comment on the comments I couldn't. Please forgive me - I'll try again from home (keep forgetting).

Posted in

Just Thinking

|

4 Comments »

April 23rd, 2007 at 09:04 pm

I don't have anything to add. But I just had to say it has been kind of dry over here. & I just wanted to say I am excited as my busy season draws to a close and I can get cracking on Craigslist and ebay and all that. I plan to be adding a lot to my challenge in the next few months.

I don't really mind losing momentum the beginning of the year because my overtime bonus is usually my biggest windfall for the year. So I haven't done a lot of little things but I got a big check for my hard work. But now I can focus on pinching pennies a little more. I am definitely ready for some spring cleaning!

Another good thing is working so much means I just don't get out much. Well, good and bad. I am trying to figure out how to work lunch back in the budget so I can see my friends once in a while. Luckily they don't mind that I prefer Taco BEll. I think I am going to start tending to meet my friends for simply a soda or something - I can eat before I meet up with them. It is a new strategy in staying social without spending a lot of money. Lunch time is frankly the only time usually I can keep up with them so I am not keen on dropping friends when I can just alter my habits a bit. Just in recent months I have been using that eat out money elsewhere I guess - who knows where it's been. I have just been trying not to go to the ATM but only have had $2 in my wallet for the last couple of weeks. Guess I usually go to the ATM more... But it's been nice in a sense not having to. But man I feel like I have been living under a rock too.

Posted in

|

1 Comments »

April 23rd, 2007 at 01:27 pm

I am enjoying seeing the blogs come to life with so many pictures.

WE decided to go for a walk last night and I decided against dragging along the camera, but when I stepped outside I Saw this, so ran back in for it.

Picture #4

If you look really closely, the lower right-hand corner of the clouds has a faint rainbow.

& then the sunset progressed.

For the area, not the most spectacular sky or sunset. It gets really beautiful in the evening as a rule. & the sky has just been so beautiful with a brilliant blue and puffy white clouds in recent weeks as well. But overall a pretty nice evening. We stayed out for an hour and the rain cloud seemed to shift south, stayed clear of us - phew. I got some well-needed exercise. Have to enjoy before it starts getting hotter than Hades... But even so we are lucky to be near so many water ways, it tends to cool off in the evenings with a breeze, but not always. Yup, definitely enjoying mild weather.

In other news, I think we are going to give it a test with the $10k credit card debt, 0%, to earn interest in the bank. I think we just felt uncomfortable borrowing more money than we had. No particular reason, it is just a lot of money to mess with if something goes wrong. What? I don't know really. But the original $20k seems a bit much. I think I will try to get $12k, so even as I pay down the minimums, the $10k will earn interest. Dh has been firmly against investing our e-fund at all as is, but now he is like, maybe we should invest a bit. Is he crazy? LOL. We can take the money we earn from it and invest it - fine. Sometime I just don't know. Why look over a 5% "sure thing"? But anyway, we already expect to earn $500 this year from our rewards card, and now maybe $500 from this little ploy. I think after we give it a try we will try for another Citi Card and see if we can get another balance transfer. I have no idea how much they will give us, but I am sure they won't blink at $10k with our credit score. I think we will open one in my name and one in dh's name just so it won't really hit either of our credit scores very hard. Frankly, in our situation, I think it will help. Anyway, I think I am a little weirded out by the idea so we'll test it and get our little $50 gift card (woohoo). & if I don't regret it and just pay it back in a couple of months - LOL - we might try to borrow a little more. Free money here we come. We have been pondering it, and I just don't feel comfortable opening a lot of cards just for promos and how it could mess with your credit score. But if we can open 1 each, play the game, and close the cards without much of a blip to our credit score, then I am in!! Which I am sure we can. I just am not sure we can do this indefinitely. So I don't want to get too used to it. But all the same I feel quite pleased at the idea of making $1k off the credit cards in 1 year. Doubling our current returns. Well, maybe even tripling if we can get 2 cards at $10k. We'll see!

Not only does CitiBank have no fees and all that, and the gift card promo, etc. BUT the best part to me is just being able to get a check deposited directly to my money market account. I still do not trust the credit card companies enough to send a big negative balance to them I guess.

If you told me a year ago I would apply for $10 cc debt, I would have thought you were insane. Oh yeah - this is going to add to my challenge money - woohoo.

Oh anyway, here is the blog where I got the idea (below). I considered it carefully because I do not necessarily agree some of this bloggers' money-making ideas. For one, I can't see myself applying for a zillion cards just for free money and promos. It has got to affect your FICO signifcantly. But we'll see. I was also reading his step-by-step guide to investing in Treasuries, which was very useful and interesting, I do have to say. But just left me not seeing the point because I can make more in my money market with a lot less effort. But I will keep in mind for when times change. So I had to look at this cc idea a little more critically, and I still think it is good as long as you don't overdue it. So while I recommend the blog overall, I wouldn't do everything the guy suggests myself. I guess a reminder to consider things very carefully when it comes to finance.

ETA: Oh, to give the guy credit he seems pretty on top of the credit score thing - I just saw more of his replies on the subject). I guess the risk is not my thing - LOL.

Yes - for Citi the fees look like they are waived on most of the promo deals for most cards right now. But I will definitely let you know how it goes - will keep you updated.

Text is http://www.mymoneyblog.com/how-to-make-money-from-0-apr-balance-transfers/ and Link is http://www.mymoneyblog.com/how-to-make-money-from-0-apr-bala...

Posted in

Budgeting & Goals,

Picture Project

|

4 Comments »

April 20th, 2007 at 06:32 pm

Well you might want to skim my last post/rant to get up to speed. But this is where I admit I can be a little jekyl and hyde - LOL.

I called my mom and gave her the spiel. & she was like, righ on sista - what is wrong with your hubby? & then after ranting and raving for a bit I said, you know, I hate to admit it but I am kind of excited. Dh kind of sold me on the HDTV a long time ago and I have been wanting one. It is not ALL him. So I kind of admit that and our conversation was so funny. From "what a doofus" and "what is he thinking???", to us being kind of excited. My mom said, yeah, she can't wait to see it - LOL. & then she said, "you know, I know you will enjoy too, just take the money we gave you to buy it and don't worry about it. Would you like a loan even?" So from what a bum - to offering a loan. LOL. I said no. But it was kind of funny. I even admitted to dh I wasn't all that upset - as long as he makes an effort to pay for it on his own accord. I know he could bring in some money if he tried. For one he still has an old projector to sell. Is all I really ask. Maybe this is the kick in the pants that he needs. But I didn't let on that much either - he needs to know I Am serious - we can't just do this all the time. I can pretend he is really in the doghouse for a while. He is in a sense. These t.v.s are coming down in price - other sales will pop up - he could have waited, honestly.

AH, you see he has wrapped me under his spell. I actually just have rolled my eyes at his precious t.v. through the years, but a few years back (2003?) his uncle got a big fancy HDTV and I was awed. The first time I really *got* any level what is so special about an HDTV. I think it was then he sold me. Thought back then he wanted to spend $10k on a HDTV and we compromised with the projector which is twice as large as the biggest t.v. & cost 1/4 as much. So has been our compromise through the years.

Anyway, we had been talking about buying a $700 or so t.v. for upstairs - a more modest t.v. - dh has been manipulating me because I am blind and we have tiny old t.v. up there - so he has been pushing the angle of getting a nice, much bigger HDTV up there, one I can see and read without my glasses. & the t.v. signals are all converting to HD in a couple of years anyway, so he was selling me. We were considering it with Christmas money, keeping an eye out on a deal for this particular t.v. - he already had one picked out. So in the end just $300 more for the perfect main t.v. Not the worst. He did offer to sell the old one and I said no way - we should move it upstairs so I can see the t.v. in bed. Then we just won't have to upgrade that one. Makes more sense. The other t.v. is his baby and he made a really good purchase he is still pleased with - only thing wrong is it is NOT HDTV. LOL. It was the first big purchase we ever made together. Well, after our first home. & well it cost about $1500 - so much more than this HDTV which is about twice as big - too funny once I think of it that way. That in the end his first HDTV costs less than that baby.

Of course downstairs renders our old entertainment center null and void. So we still have to work it out. & I have a fear it won't be too long before there are talks of upgrading our free TIVO to HD. Which is another reason why we have passed so long on uphrading the main t.v. to HD - in no hurry to upgrade our TIVO since it is free in the interim - and is mostly how we watch t.v. - through the TIVO.

So, many problems are presented. But hopefully dh will get a job to pay for all this crap. & I have to admit I am kind of excited we now have a 50 inch HDTV. It is pretty sweet. I have been surfing the web and they generally run $1600-$3k so I kind of see dh's angle on the deal. Believe me he has been waiting years for a deal like this. & to have the windfall to pay for it. It isn't all bad. I guess.

Oh yeah my only other concern is that it is rear-projection as well. So I was asking if that meant it had bulbs that burn out with time, like his projector does. Yes, the bulb should last 10k hours. He cracked me up though becuase he said he thinks it will help him watch less t.v. Yeah right, who is he fooling?????? Whatever!

Anyway, the kids are ALL excited. My eldest keeps telling me that daddy bought a GIGANTIC t.v. LOL. He thinks it is pretty cool. All I have to say to that is I apologize in advance to my sons' future wives.

Posted in

Just Thinking

|

5 Comments »

April 20th, 2007 at 03:50 pm

Okay, he has only done something SO stupid once in our marriage.

Anyway, irony is I was teasing him about his stupid PS3 and how he just had to have it and wouldn't spend a dime otherwise all year, but well he has spent a few dimes otherwise - LOL. So I already blogged, that I am sure he could do it, he doesn't usually buy much at all. BUT at the same time, how long until the next best thing? He got super aggravated with me for teasing him...

Well anyway, it was 2000 when we were getting ready to move into our big house, and saving our pennies for a down payment, wondering if we would be able to sell our old home, etc., when he went out and bought a $2500 projector. We had only been married a little over a year but I thought we were seeing pretty eye to eye. But honestly, I don't even think he asked me. It was like, BTW I ordered a projector. BEcause it was a deal TOO GOOD TO PASS UP!!! He was sure it was a typo and he didn't really think it would go through or something (ordered online). Yeah, I Was livid. Anyway, back then we really had more money than we knew what to do with. So as annoying as it was. Mostly the principle that he made a $2500 purchase without telling me. Whatever. Believe me he has done nothing like that anywhere close since.

But this morning I Was laying in bed. I had gotten up and done my "How To" post at 4am because I couldn't sleep. & then I tried to go back to bed (felt pretty wide awake) around 6 because had gotten no sleep the night before (baby had a horrid night). I figured I really needed sleep. Well, I did. Dh came and tried to wake me at 7am, and I said no way. So he woke me up again later and I was pretending to sleep - I just did not want to wake up - LOL. But oh yeah - he had a way to wake me up. HE says, "How much do you love me?" Oh lord, I am thinking. I am awake now. So I open one eye to show I am awake. "What now!?!" So he proceeds to tell me there is a HDTV on sale at Fry's for $1k and he HAS to have it because there has never been such a deal on such a t.v. Being a realist I am just like, no way in hell. In 2 years we can buy something twice as good for 1/2 as much. But then he keeps insisting that no - this t.v. is such a good deal, we will never find a t.v. anywhere on par for this cheap ever - not even in 2 years. I am just rolling my eyes at him. But clearly something in his being has to have this t.v. and I do love him. So I told him pretty clearly he could buy his precious t.v. but he has to get a job to pay for it because my wage simply can't support it. I told him, he was killing me, on top of my job and overtime I was bringing money on the side. & I Was frankly tired of doing all this not to get ahead but just buy him more crap. When was the last time he brought in a dime?

So he runs off to the t.v. store and I am just annoyed right now. Then of course he starts saying we need a new entertainment center and blahblahblah. IT never ends!!! My god!

You know if he would get a job it wouldn't be as big a deal. HEck, I would like it if he would. If he would keep it to fund our retirement a little too. But today I am just really skeptical if he will come through. He insists if he buys it he should be able to sell it at a profit if we change our minds. So whatever. I know the odds are slim he would give it up. But the clock is ticking on the best deal ever had, so it is buy now, think later.

& you have to understand projector #1 was to curb his appetite for HD? IT has, but so did projector #2 which is barely 2 years old!!!

I am just extra annoyed because we just paid off the car. I just wrote the check. Could this have come up a week earlier? We just came into a lot of money. But why does he get to spend it all and I am left to square one, worrying about how to fund our retirement?

Mostly I think this means that preschool is entirely out the window for the little one. I had set aside about $1k for that, to give dh a little break. But uh uh. HE doesn't deserve it. I am sorry that LM can not go hang out with his brother and all one day a week, but apparently a t.v. is more important than anything. Gah.

I only hope and pray it is such a good deal there that there are no more left when he gets there. So he doesn't have to work a job all summer to pay for a t.v. when he couldn't even get a job to pad our retirement a little.

Apparently he has the 7-year itch. 7 years since he pulled this crap. Anyway, I know I have been very, oh ,we always see eye to eye and discuss things. I think this is just a little bit much because he just got his stupid very expensive PS3 too. It is just too much right now. He is driving me absolutely insane! Thank god he doesn't always pull crap like this. But well, he is wearing on my last nerve.

The thing about us is that through college I lived on my own and footed most the bill. He didn't work any less hard - he was always working many jobs, but he stayed at home and had no bills, so had completely 100% disposable income. & he really got to keep up a lot of that lifestyle when we first married. But frankly, he just doesn't *get* that he has to choose. That is what it comes down to. We agreed to live on 1 income and have a more relaxed lifestyle. But suddenly the rules are changed. Suddenly he wants to spend his nights and weekends working so he can keep up this lifestyle. & though I would feel better if he would just get a job. IT aggravates me all the same. Sometimes I wonder if he could really live through tight times. He is frugal, he works hard, he never buys with debt, etc. But he is not getting that though cash is in the bank, it is not there to spend! Sometimes I am amazed he did not come out a bigger spoiled brat the way his parents handed him so much, and times like these I see that he has - he is a big spoiled brat. He got a lot of the work ethic, be frugal, buy cash, etc. But mix that in with a little spoiled and there you have it. A guy I can live with on a tight budget 90% of the time, but who every once in a while, his brain goes entirely out the window. Seriously this is the guy who nagged me about eating out at Taco Bell last weekend when we could pack a lunch and I told him not to start with me, if I wanted to spend $10 at Taco Bell for a family meal I darn well was going to - LOL. I was annoyed he as nagging me baout a small splurge when he had just bought his PS3.

So I don't know, could I have said no? Well, I did try to say no. We'll see how it turns out.

Posted in

Just Thinking

|

5 Comments »

April 20th, 2007 at 12:27 pm

When shopping for a used car you can take two very different routes. In my younger years with much less cash I always bought used from a private party. But you can also find some pretty good deals at the dealer as well.

When shopping for a used car you could start with your newspaper, or better yet try something like Craigslist. Don't limit yourself to your immediate area if you travel often or have family in areas a little farther out. Increase your options.

Secondly, you need to come up with a list of questions to ask about the car. Some things that are important:

1 - Condition of Car

2 - Does it have a salvaged title?

3- How many miles are on the car?

4 - What are the features on the car (sound system, type of engine, power doors and locks?, etc.)

This is usually my preliminary list. It is impossible to tell if a used car listing is a good deal until you gleam this information. If the deal still looks good after these questions are asked, then make an appointment to see the car and do a test drive.

Two notes. I would never buy a salvaged car. The reason though is in this area there are plenty to choose from at very low prices that have no dings in the title. Just keep in mind even if you are willing to buy salvage, how will it affect the resale? If you have no other options you might find a steal. But I don't know much about salvaged titles than that I personally steer clear.

Secondly, in California a car has to pass Smog inspection before it can trade hands. Other states may have similar rules. In California that is one of the first questions I ask - if a car has been smog checked recently. If not, it's okay, as long as the seller takes responsibility to get it done. & then before the car trades hands I Would personally get it smog checked again myself. It is easy to fake a passing and one of my worst car buying experiences involved a fake smog check. But it was our follow up that helped us to decide that we didn't want to do business with his character. Never buy a car from someone once you find trickery is involved. I made this a simple rule in the future to help not to fall for a bad car deal.

Anyway, what kind of car should you look for? When going used there are two very different angles you can go. You can buy a really old Toyota, Saturn, Honda with a lot of miles and get a really nice car in the $1k-$3k range. The two best cars I ever owned were a Toyota with well over 150k miles (lasted 7 years with very minimal repairs) and a Saturn with about the same amount of miles (this one I used as an interim car when I wasn't ready to shell out the big bucks on a large family car, which was a long-term goal, but when I finally realized convertible and new baby don't mix). Those are the car brands I lean towards due to longevity and relative lack of repairs. When you can buy a $1k car for a few years and sell it for $500, never having spent more than a couple hundred of years on a repair, you have it made. These cars are of the safest and most reliable. Plus, if you do get a bad deal, you aren't out too much money.

On other end of the spectrum you can find a car that is a lot newer. A particular steal I always look for is a car that is an older make, but a car that has been mostly garaged and has few miles. I bought a 1992 Ford Mustang convertible in 1999. It had been driven so little it still had a new car smell and as absolutely immaculate. At $5k you can't find a much better deal for an all but brand-new car.

Once you pick out a car that sounds good on paper, make that appointment and test drive it. For the convertible I took it through the car wash to test for leaks. I generally found car sellers were fine with you taking the car for long test drives and visits to your mechanic. Any seller who isn't is one I would not deal with.

If the car drives well, check the car inside and out with an eagle eye. Always check the oil and fluid levels. Look for obvious signs that the car has not been maintained. I generally have found over the years that people that maintain their engines also keep their cars immaculate. The more immaculate the car inside and out, the better you can assume it has been well taken care of. I have looked at cars that had little (very old) oil but the car was trashed anyway. The two really seem to go hand in hand. But if you come across someone who is a neat freak but not big on maintenance, a quick look under the hood will give you some clues. Also, check the body very carefully. Body damage is often obvious if you just look closer. Always ask if the car has been in any accidents too. This is a huge area to consider and to have your mechanic look at (hopefully one who specializes in body work).

Of course the next step is to ask how many owners the car has had and if the seller has repair and maintenance records. & ask if you could take the car to a trusted mechanic (or something like AAA) to have a once over from a car professional. I have never had anyone say no to this.

Generally, from there, if the car is good I would negotiate a price, dependent on outcome from my mechanic's check. Just keep in mind that people selling cars are usually asking too much. Before you look at the car you should look up the blue book value (www.kbb.com) and see what a good price is dependent on the information you have. In years past a general rule of thumb was an average between wholesale and retail, but these days kbb.com also shares private party values, which is where you want to look. The general rule of negotiation is they start high, you bid low, and a compromise is made. However, not all car sellers are negotiators. I have had many people tell me what the least amount of money they would accept was (well below blue book or asking price). If someone tells you that, jump on it. In the end though, ask a price that is reasonable, but keep in mind that if there are 50 cars for the same make and model and year listed in the paper that the seller has to be pretty desperate. Adjust downward a bit if you get the feeling the car has been sitting a long while. & if you just can't agree, walk away. Either it isn't worth it or you may just be able to call a bluff. For a rarer car of course, you may have to offer a little more. My general experience is sellers like to act like they have buyers lined up and the reality is they don't. Living in the big city myself, there are just way too many used cars to go around.

The final step once you agree on price (& after the mechanic check) is to exchange money and transfer title. In California you can not sell a car without a "pink slip." So make sure they have the proper title and documentation and are able to sell their car. Go as far as to check their ID, that it matches the title. You can never be too careful when buying used. Whenever we have bought a used car we have always written up a small contract with the purchase price and had the seller and buyer sign. Doesn't have to be anything fancy. But just something in writing to defend yourself. A written contract is better proof than an oral contract if a dispute arises from the sale. I find it best to do an initial contract, and probably redo it if you have to further negotiations after a mechanic check. Regular repair and maintenance is not a reason to walk away from a deal, but you can have the seller pay for the work, or adjust the price downward. After my bad smog check experience I usually rather bargain on the price and let my trusted mechanic do any work that may be needed.

There you have it, a used car on the cheap. Our family has bought so many used cars using this method and have been blessed with many great deals, so I generally don't have the fear of buying used that most do. But of course, by being slow, careful and methodical you can weed out most of the bad deals pretty easily. I think the biggest rule of thumb is just never rush into anything. When a seller is rushing you, something is wrong. Don't fall for it. There are plenty of other fish in the sea.